March has been a turbulent month for all investors with the Dow Jones Industrial Average experiencing two of its top five largest daily percentage losses in history. The nation is in shutdown mode with shelter-in-place orders, and the unknown outcome of this pandemic is creating emotional and economic turmoil. The initial effects of COVID-19 and its impact on investing in the industrial sector is still not yet fully known. While the landscape remains uncertain, there are several key takeaways from the turbulence all have experienced this March:

- E-Commerce adoption and penetration have accelerated

- Resiliency of supply chain will take priority over just-in-time efficiency

- Near-shoring or on-shoring manufacturing will benefit key certain submarkets

- The so-called denominator effect may impact allocations to private real assets

- Debt markets are unstable which will have unintended consequences

- Real estate investors are re-pricing risk

- The impact of rental rate decreases on industrial assets is a real possibility

E-Commerce

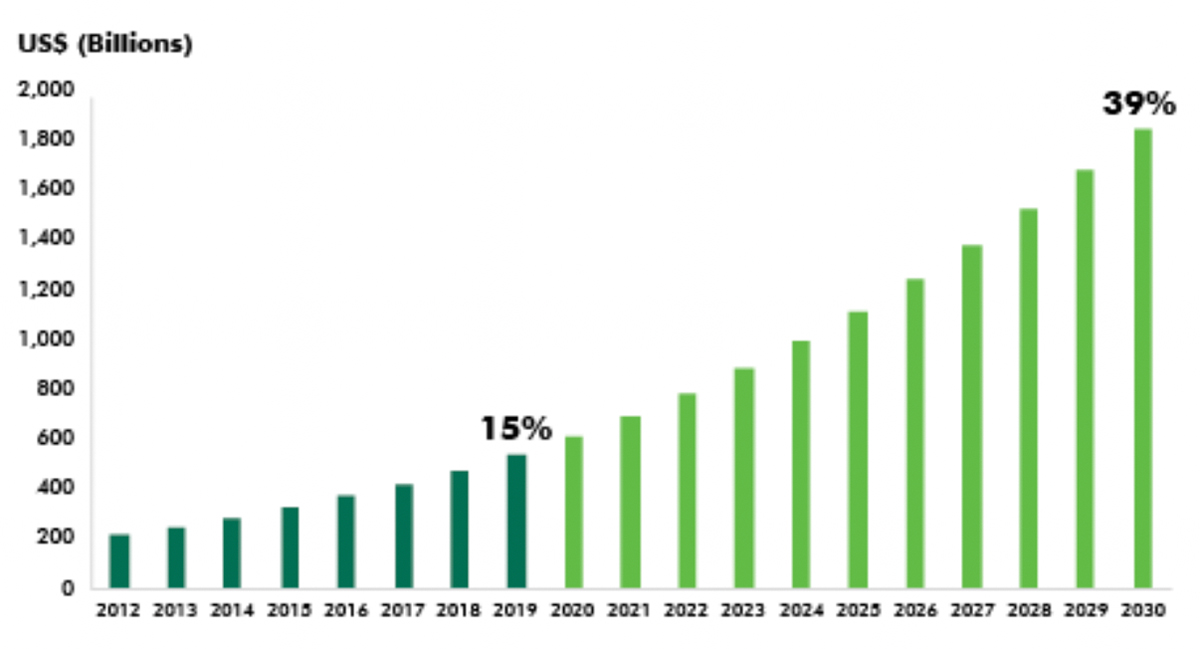

E-Commerce has been the leading demand driver for industrial real estate since the Global Financial Crisis (“GFCâ€). Indeed, with many cities, malls, restaurants and general retail establishments closed as a result of COVID-19, e-commerce users have benefited from increased online shopping during this time. An unintended consequence of the virus is the acceleration of e-commerce penetration into the overall retail sales market. According to CBRE, in 2019 e-commerce sales exceeded $600 billion and accounted for 16% of all US retail sales. We believe this increased adoption to e-commerce will continue after the pandemic passes and industrial buildings will benefit from this ongoing structural change.

FIGURE 1

U.S. E-Commerce Penetration, % of Total Retail Sales Forecast

Source: Post-Coronavirus Industrial Real Estate Market Flash, CBRE

Supply Chain

Since the GFC, companies have focused on just-in-time deliveries with the goal of managing their overall inventory in order to reduce costs. However, we anticipate that companies will move away from the just-in-time inventory management system and focus more on their supply chain resiliency and redundancy. This may create another potential demand driver for industrial real estate should companies want additional inventory to withstand unexpected shocks. According to RCLCO, a highly regarded advisory firm founded in 1967, a 5% increase in total business inventories could translate into the need for an additional 500 – 700 million square feet of industrial space nationwide.

Manufacturing

Given the supply chain disruptions caused by COVID-19, it is possible that companies may investigate moving or supplementing their manufacturing in China – and elsewhere across the globe – to locations closer to the American consumer. Previous to COVID-19 the efficacy of manufacturing solely in Asia was declining relative to other parts of the world and these recent events may be the impetus for companies to adjust their manufacturing processes either on-shore or near-shore. Should this manufacturing shift occur, gateway markets such as San Diego and Phoenix and states with lower labor costs, such as Nevada, may stand to benefit.

Denominator Effect

In our last letter we described the denominator effect and the potential it may have on institutional capital sources investing in real estate. Our forecast two weeks ago seems prescient as multiple pension funds and endowments have since indicated their allocations to real estate are now in-line or above their target ranges whereas before the recent stock market decline these same institutions were underweight. This denominator effect reared its head during the GFC and it may impact future allocations to real assets. However, should either the stock market regain some of its value or their real estate portfolio decline, then some institutional capital sources may once again be under-allocated. The relative strength of industrial real estate should be a bright spot amongst institutional portfolios and, as a result, receive an overweight in their real assets portfolio in the near future.

Debt Markets

The debt markets are in transition and are essentially illiquid.  There are now multiple examples over the last two weeks where lenders refused to fund on closing day. The Mortgage REITS (aka Debt Funds) have been the most impacted and there are rumors that some may declare bankruptcy before the end of April, or earlier, if market conditions do not improve. With our lower leverage philosophy, debt funds are not a lending source for CapRock Partners Industrial Value-Add Fund III, but this disruption in the lending environment has already created ripple effects to traditional lenders. As a result of these ripple effects – even though both LIBOR and 10 Year treasuries are declining – the overall cost of debt is increasing since spreads are widening and all lenders now have a 10 Year Treasury or LIBOR floors.

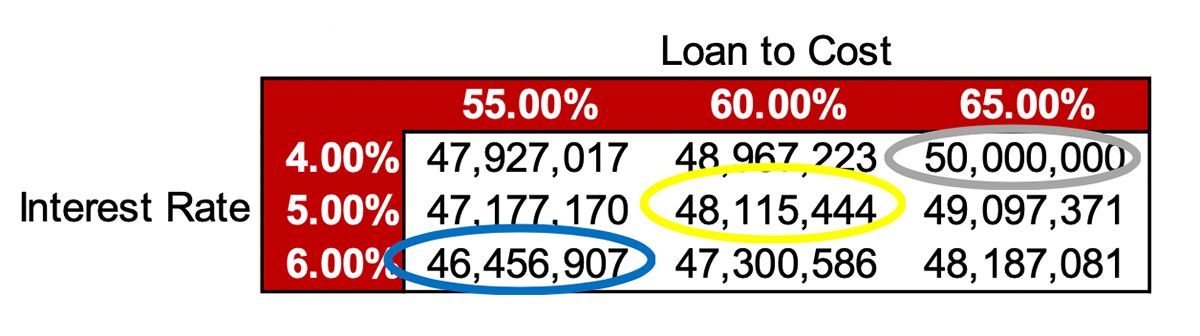

More impactful to equity returns and the overall value of real estate, lenders are curtailing proceeds to reduce their risk in an uncertain environment. Depending on the characteristics of the deal and the lender profile, we are already seeing lenders reduce their loan proceeds from 65% to 60% LTC or from 60% to 55% LTC. A major determination of real estate value is the anticipated equity return on a given asset. All other things being equal, with the reduction in loan proceeds there are two options: the investor accepts a lower anticipated equity return or real asset values decline. The below is an example of how the reduction in proceeds coupled with an increase in interest rates impacts the value of real estate (all other assumptions constant: lease rate, absorption, exit cap rate, etc.).

EXHIBIT A

Price required for project level 18% levered IRR

Assuming an originally underwritten $50,000,000 purchase price with a 65% LTC and a 4% interest rate (300 spread over 10 Year Treasury with 100 bps floor) the above chart summarizes:

- +/- $2 million purchase price reduction (+/- 4%) would be needed to maintain an 18% LIRR (“Levered Internal Rate of Returnâ€) in the event of a 5% reduction in LTC proceeds (from 65% to 60%) and 100 bps rate increase (from 4% to 5%), as shown in the reduction from the grey circle to the yellow circle.

- +/- $3.5 million purchase price reduction (+/- 7%) would be needed to maintain an 18% LIRR in the event of a 10% reduction in loan proceeds (from 65% to 55%) and an a 200 bps rate increase (from 4% to 6%), as shown in the reduction from the yellow circle to the blue circle.

Equity Investors

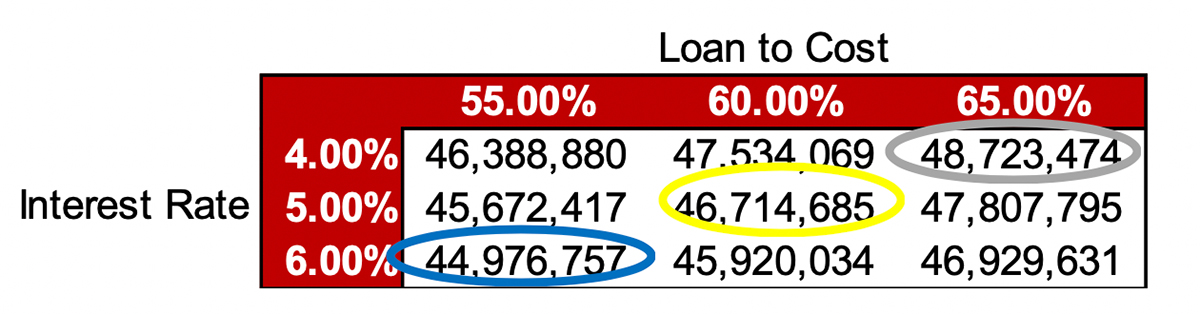

In light of the economic climate and the increasing probability of a global recession, equity investors are re-pricing risk and are demanding a higher return. Equity investors who may have been satisfied with an 18% LIRR before the pandemic are requiring an additional risk premium of at least 200 bps in order to pursue deals with any perceived risk. This increase in risk premium, coupled with the reduction of loan proceeds, will serve as a double impact on real estate value – even if NOI does not decrease from pre-pandemic levels. The chart below incorporates the reduction in loan proceeds from EXHIBIT A but layers in the equity investors 200 bps increased risk premium demand, from an 18% LIRR to a 20% LIRR.

EXHIBIT B

Price required for project level 20% levered IRR

Assuming the same originally underwritten $50,000,000 purchase price of EXHIBIT A, with a  65% LTC and a 4% interest rate, EXHIBIT B summarizes:

- +/- $1.3 million purchase price reduction (+/- 2.5%) from the original $50 million value is necessary even when maintaining 65% LTC and a 4% interest rate simply as a result of the 200 bps increased risk premium, as shown with the grey circle.

- +/- $3.3 million purchase price reduction (+/- 7%) from the original $50 million value would be needed to maintain a 20% LIRR in the event of a 5% reduction in loan proceeds (from 65% to 60%) and a 100 bps rate increase (from 4% to 5%), as shown in the yellow circle.

- +/- $5 million purchase price reduction (+/- 10%) from the original $50 million value would be needed to maintain a 20% LIRR in the event of a 10% reduction in loan proceeds (from 65% to 55%) and a 200 bps rate increase (from 4% to 6%), as shown in the blue circle.

Â

Â

Rent Declines

Industrial real estate continues to have several demand factors but it is imprudent to believe that industrial – insulated though it may be – will not have rental rate declines in certain segments if there is either a global or US based recession. While industrial real estate should fair better than other real asset classes that does not mean it is immune to rental rate decreases.

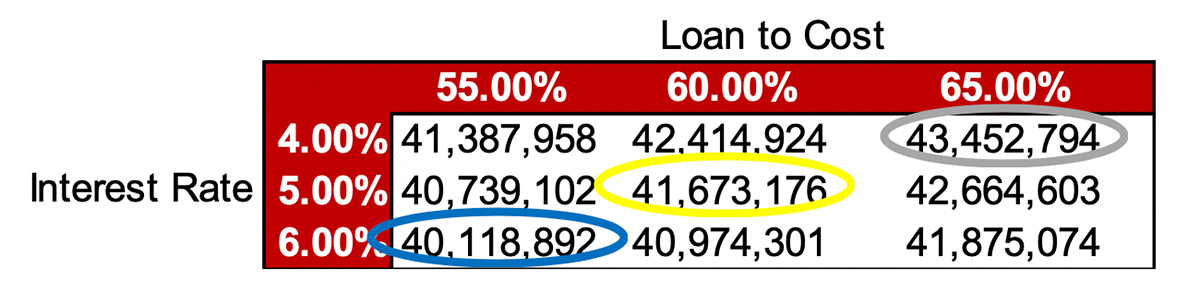

At CapRock, we are focused on the possibility of rental rate declines in certain size ranges and credit profiles. Rental rate declines, combined with both a reduction of loan proceeds (EXHIBIT A) and an increase in risk premium (EXHIBIT B), will significantly impact real estate value.

EXHIBIT C

Price required for project level 20% levered IRR with 10% rental rate decrease

EXHIBIT C shows the impact of Net Operating Income (NOI) declines in light of both the reduction of loan proceeds (EXHIBIT A) as well as the increased risk premium investors are demanding (EXHIBIT B).

- Assuming a NOI decline of 10% across the portfolio and investor expectations for a 20% LIRR the original $50 million price needs to be reduced to $43.4 million (+/- 13% reduction) even if the debt remained at 65% LTC with a 4% interest rate, as shown in the grey circle.

- +/- $8.3 million purchase price reduction (+/- 16.5%) would be needed to maintain a 20% LIRR in light of a 10% NOI decline with a 5% reduction in loan proceeds (from 65% to 60%) and a 100 bps rate increase (from 4% to 5%), as shown in the yellow circle.

- +/- $10 million purchase price reduction (+/- 20%) would be needed to maintain a 20% LIRR in light of a 10% NOI decline with a 10% reduction in loan proceeds (from 65% to 55%) and a 200 bps rate increase (from 4% to 6%), as shown in the blue circle.

These are theoretical examples since NOI typically does not decrease by 10% immediately given the typical long-term leases in industrial real estate. Nonetheless, it is imperative to view real estate investing in light of the COVID-19 pandemic through a lens of less loan proceeds (EXHIBIT A), a higher risk premium given the uncertainty (EXHIBIT B) as well as the very real possibility in certain segments of a decline in NOI (EXHIBIT C). When leases expire there is no certainty that the next lease will be at or above the previous rental rate and hence a decline in NOI is a possibility for the first time in a decade.

CapRock Partners Industrial Value-Add Fund III is well positioned to invest through these uncertain times. We started the company during the depths of the GFC and we have a proven ability to navigate successfully through both strong economic times as well as uncertain ones.

We continue to thoughtfully and prudently evaluate the investment market and believe there will be unique buying opportunities in the months to come. Unlike the public markets, it typically takes a period of time for signs of cracking to emerge in real estate, and while industrial may not have the same distress as other real asset classes, we are prepared to invest when the correct opportunity presents itself.