It has now been more than 100 days since the coronavirus pandemic hit the U.S., and industrial markets seem to be adjusting to the perceived new normal. Much of the country remains on lockdown, with some states pausing or rolling back their opening plans. While the path forward as a nation remains murky, it has become apparent that some asset classes are better positioned to weather this unforeseeable downturn. Industrial real estate has emerged as one of the most resilient real asset classes, and investor appetite for industrial real estate has increased. While the effects of COVID-19 and its impact on investing in the industrial sector are not yet fully known, some conclusions can already be drawn:

- Cap rates for core industrial deals will compress

- Debt is now available for select deals, albeit at lower proceeds than pre-pandemic

- Tenant demand in the Western U.S. remains robust

- The denominator effect does not seem to be an issue given the public equities rebound

- Reduced U.S. dollar hedging costs may lead to an increase in international investor interest

Cap Rates

During the first three months after the pandemic took hold in the U.S., industrial capital markets were essentially frozen with few transactions occurring. Buyers were cautious given the uncertain environment—recall the Dow Jones Industrial Average experiencing two of its top five largest daily percentage losses in history in March—whereas sellers were still expecting year-end 2019 values.

As more data emerge, it is clear that not every industrial deal is created equal, and a marked divergence is materializing between core investments and non-stabilized properties. Many investors anticipate persistent uncertainty in the near future and are chasing stabilized investments secured by credit tenants at cap rates lower than year-end 2019. These core buyers tend to be all-cash buyers, ergo, are not affected by the turbulence in the debt markets. In addition, they have not been able to deploy capital for approximately 100 days and are looking to reallocate capital from other underperforming real asset classes such as retail, hospitality and office. As a result, the demand for stabilized product will continue to compress yields. For these reasons, this might be the best time to sell a core stabilized industrial investment for some time. On the other hand, the market for non-core deals needs more “price discovery.†In addition, value-add transactions have come to a sudden halt due to a lack of debt financing for this product type.

Debt Markets

The debt markets are still in transition and remain bifurcated, except for stabilized investments. Although seemingly each week there are additional lenders dipping their toes into the marketplace, it is abundantly clear that the proceeds for value-add investments will be reduced for the foreseeable future. The lack of loan proceeds is resulting in a bid-ask spread between sellers who are holding on to the 2019 value of their non-stabilized investment and buyers who are underwriting a lower valuation given the reduced loan amount. To be clear, it is not necessarily uncertainty about lease rates or absorption timing—although prudent investors are factoring in both—that is contributing to the bid-ask spread and lack of value-add transactions. Rather, it is primarily the lack of loan proceeds.

When the debt markets thaw, more value-add transactions will resume. Until then, the bid-ask spread will persist unless sellers capitulate.

Tenant Demand

The demand for industrial space in the Western U.S. over the last 100 days seems nearly unprecedented. A variety of factors may be contributing to this surge, including increased e-commerce adoption, the need for additional inventory to withstand supply shocks, the resurgence of domestic manufacturing and the fact that retail tenants need more space to warehouse their products since traditional retail stores remain closed. And, it is worth noting that this is a broadbased tenant demand, not limited to only Fortune 500 caliber companies. CapRock is experiencing additional demand from a wide range of businesses, including e-commerce tenants, manufacturers, retailers and traditional third-party logistics (3PLs). Additionally, given the breadth of our portfolio, we are signing leases ranging from less than 10,000 sq. ft. to more than 1 million sq. ft.. Rental rates remain strong and with seemingly more tenants in the marketplace today— at least in the Western U.S.—these rental rates have remained steady for buildings larger than 100,000 sq. ft. and landlord concessions are not materially different than pre-pandemic.

Denominator Effect

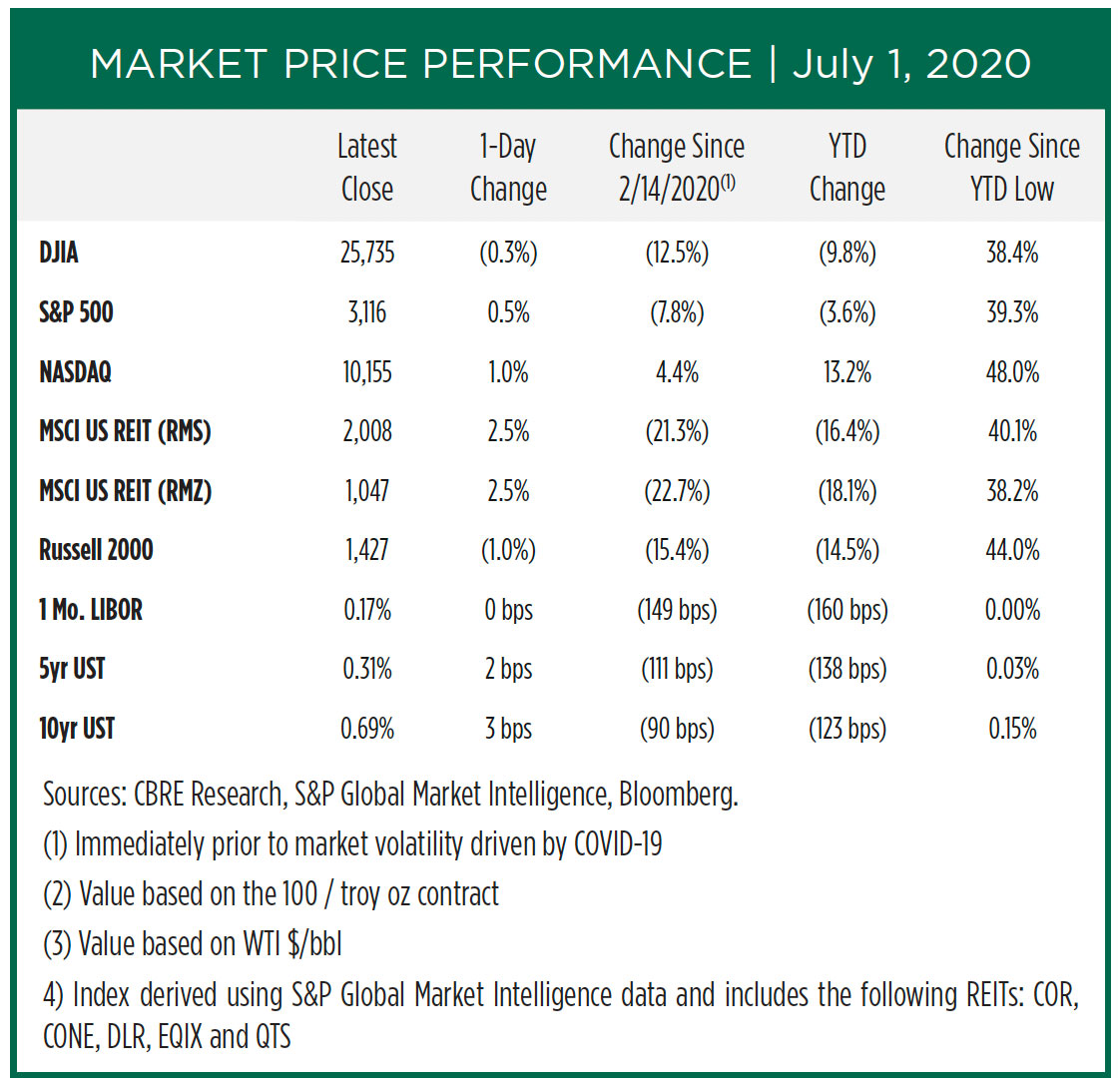

At the onset of this pandemic, when the stock markets plunged, many investors were concerned about the so-called denominator effect, which often leads to an overallocation for real assets in their overall portfolio, and potentially requires them to either pause new commitments or sell some of their real asset investments in order to maintain their targeted allocations. As illustrated in the chart from CBRE, the significant rebound in the Dow Jones Industrial Average (DJIA) has mitigated most of the fears about the potential denominator effect and, as a result of this rebound, institutional investors have not been forced to reduce their allocations to real assets. As of July 1, 2020, the DJIA is only 10 percent lower than its January 1, 2020 levels and 38.4 percent above its market low. And, despite the pandemic, the NASDAQ is actually 13.2 percent higher than it was on January 1, 2020.

U.S. Hedging Costs

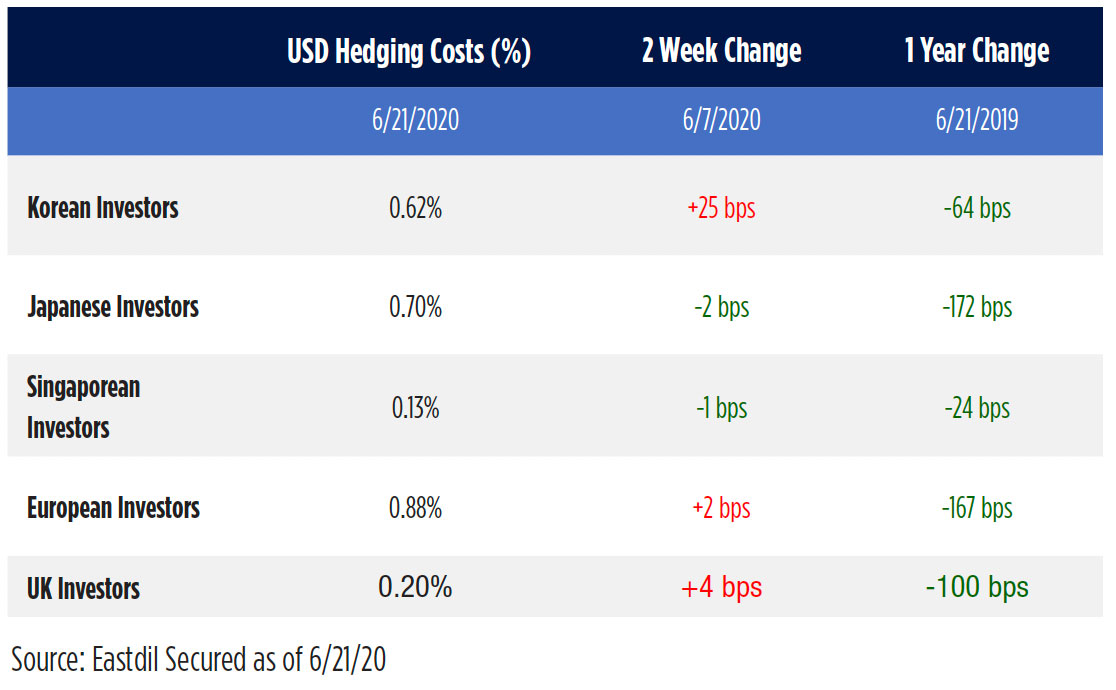

The pandemic also caused a significant reduction in hedging costs against the U.S. dollar, and it seems highly probable that international investors—particularly European and Asian investors—will re-enter the U.S. real estate market in a meaningful way. Over the last several quarters, many international investors have paused their investments in U.S. real assets given the perceived lofty valuations of many asset classes combined with unusually high hedging costs that further diluted their overall returns. As the chart from Eastdil Secured shows, hedging costs for international investors have dramatically reduced year over year, which should create an opportunity for overseas investors to increase their exposure to U.S. real assets. And with strong tenant demand and several additional tailwinds as a result of the pandemic, many institutional investors—domestic and international— are increasing their allocations to logistics.

With the global economy in unchartered territory, it is challenging to make predictions. Yet, it has become apparent that logistics real estate remains in the sweet spot for institutional capital—both foreign and domestic. With investment capital fleeing other product types the cap rates for core investments will compress, but value-add investments will continue to see a bid-ask spread until the debt markets recover more fully. Given the strength of logistic assets and the robust tenant demand, we expect international investors to increase their allocations to both e-commerce buildings and last-mile logistics throughout 2020 and beyond.

Originally published at https://bluetoad.com/publication/?m=62780&i=668491&p=16.