“Industrial tug-of-war” by Jon Pharris, originally published by Institutional Real Estate, Inc. on November 2023. Republished with permission.

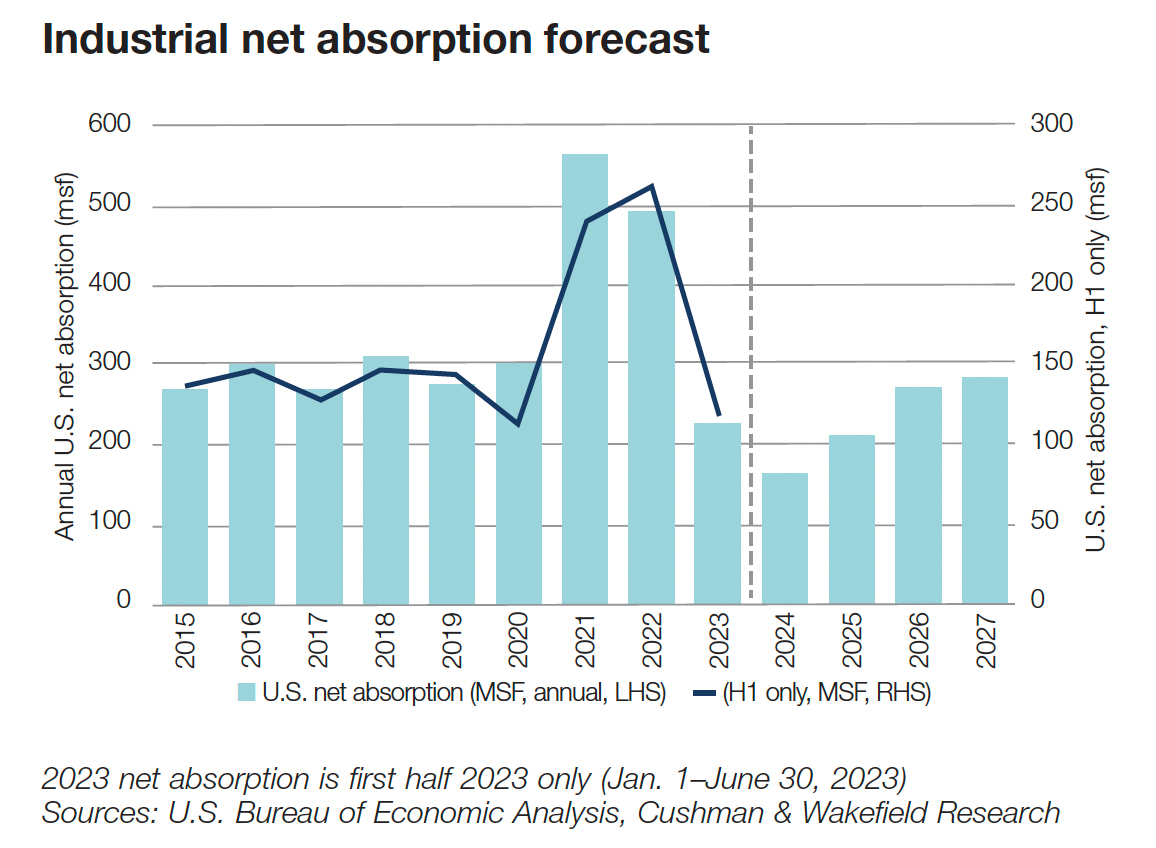

Industrial continues to be one of the best-performing sectors within the real asset class. After two years of unprecedented positive net absorption levels, tenant leasing activity is returning to more typical levels — which we don’t think should surprise any market participant. We believe the tenant demand of the last couple of years was simply unsustainable. Despite the noise about a recession or corporate pullback — which still very well could happen — 2023 net absorption is on pace to reach the third-best net absorption year on record, lagging only the record-setting years of 2021 and 2022.

Even though industrial property fundamentals remain resilient in many submarkets, capital market headwinds are reducing property valuations. The Federal Reserve’s policy shift from accommodative monetary policy to restrictive monetary policy is creating a higher cap rate environment for all asset classes, including industrial. Again, this shouldn’t be a surprise to any real estate investor, as we believe the low cap rate environment of 2021 and early 2022 was artificially induced and bound to change. That change is upon us, but it will take some time to work its way through the system.

The challenging financing environment is compounding this valuation decline. Underwriting criteria are stricter, so loans are more difficult to obtain, leverage is lower and all-in interest rates (index plus spread) are higher. Banks are also facing increased regulatory scrutiny in the wake of recent bank failures, and traditional bank lenders are often reluctant to lend even if a loan meets their underwriting criteria. Plus, many lending institutions — especially those with significant loan exposure to office and multifamily assets — are concerned about the value of their own loans.

The silver lining of all of this is that new industrial construction activity has dramatically slowed. In our view, provided tenant demand continues at a consistent pace and construction activity remains muted, the industrial market may be primed to return to a healthy supply-demand balance in 2025 once the existing vacancy and projects under construction have been leased. And there could even be submarkets and building sizes that experience a rental rate spike in the coming years because limited new product is expected to be delivered. But, of course, there may be pockets of distress where industrial owners may have been too optimistic about leasing demand or perhaps have impaired capital stack structures that are not positioned for this higher interest rate environment.

Valuation declines less severe in industrial

If more than 60 percent (at market peak more than 80 percent for some borrowers) of the capital required to acquire an asset is either no longer available or, if available, is more than two or three times as expensive as it was only two years ago, then we believe it should be no surprise that valuations will decline, all other things equal. Fortunately, industrial, unlike many other asset classes, continues to see rental rate growth, which is helping to offset some of the valuation change.

As a result of continued tenant demand projections, industrial real estate is one of the only asset classes with the tension between the capital market headwinds forcing valuations lower despite relatively positive property-level fundamentals. Industrial demand has returned to a healthy pre-COVID status. And, while tenant demand has declined from the record-setting absorption levels of 2021 and 2022, there is still strong tenant activity across most size ranges in most submarkets. In fact, over the next five years, CBRE Econometric

Advisors projects rental rate growth will exceed 20 percent for major industrial markets such as Dallas, Las Vegas, Los Angeles, Phoenix, Salt Lake City, San Francisco and Seattle. We believe this demand — provided it continues to exist — should help create a floor for industrial valuations despite the higher cost of capital and higher cap rate environment.

Industrial construction falls off a cliff

Nationally, industrial construction starts are down year-over-year and, in our view, new industrial construction will continue to decline throughout 2024 and into 2025. Real estate is a cyclical business, and we may be entering the point in the cycle where new construction may not pencil for a couple of years. We expect there will be isolated areas where new construction will be justifiable but probably not on the same scale the industry experienced over the last several years. Unfortunately, some developers may not be able to adjust to this changing business climate and may struggle to survive as their development fee revenue may sharply decline.

In contrast to previous recent market cycles, this new construction slowdown may ensure there will not be a glut of vacant industrial space on the market like we experienced in the early 1990s during the RTC or, more recently, 13 years ago during the global financial crisis.

Barring a major recession that significantly reduces tenant demand, this lack of new construction may turn out to be a positive because it will allow the market to lease through the current stock of vacant or under-construction product. In contrast to previous recent market cycles, this new construction slowdown may ensure there will not be a glut of vacant industrial space on the market like we experienced in the early 1990s during the RTC or, more recently, 13 years ago during the global financial crisis. Similar to the projected rental rate growth, this lack of new construction may also unintentionally place a floor on valuation declines and help industrial values recover before other asset classes, provided demand continues at a pre-COVID pace.

Financing activity

Financing activity for all product types is significantly curtailed from market peak, but the lack of financing is even more pronounced for assets that have impaired cash flow, such as value-added investments or new construction. The relatively few banks that are providing loans are primarily lending to premier investors or developers who have strong balance sheets and a robust roster of institutional investors. In lieu of traditional lenders, debt funds are stepping into this void, but their cost of capital is typically more expensive. It seems that investors and developers are discovering that lenders also passed Economics 101 on supply and demand.

Often, the most accretive returns are earned during market turbulence, but it can be challenging to sift through the noise and thoughtfully separate from the herd. We believe we are only at the beginning of this valuation change, so companies should be prudent and patient with an eye toward risk mitigation.

In our view, financing will continue to be more challenging — and more expensive — over the next 18 to 24 months, which will likely impact a plethora of investors who have either loans maturing or loan hedges expiring through 2025. In this environment, those who are lending are typically exploiting the higher

spreads they can charge borrowers along with higher fees and longer call protection that make it more difficult to refinance if rates (or spreads) drop in the future. On the other hand, those who have loans maturing in the near term but are unable to sell given the lack of liquidity may discover — for the first time in their careers — the term “cash–in” refinance, where additional equity will be required to refinance a loan.

Unfortunately, we don’t think there really is a light at the end of the tunnel for financing right now. We believe we are at the initial stages of a deleveraging cycle that may result in more unintended consequences.

Turmoil creates opportunities

Some investors and developers had unrealistic underwriting assumptions during the market peak and were assuming cap rates and interest rates would remain at their all-time lows. Other investors took a different approach and successfully hedged their loans where appropriate, extended loan maturities, and significantly slowed acquisition pacing during that period of irrational exuberance. Companies that maintained a disciplined and thoughtful investment approach during the market peak are now well positioned to take advantage of the coming valuation changes.

The capital market headwinds will result in distressed investment opportunities — even in industrial real estate. It is possible valuations will have a floor given the lack of new construction amidst continuing demand, but we expect there will be attractive opportunities to acquire well-located assets in high barrier-to-entry markets at prices well below replacement cost.

The buying window for value-added industrial real estate seems to be emerging on a select basis. To use the ever-present baseball analogy, we believe we are in the first couple of innings of this buying opportunity. Often, the most accretive returns are earned during market turbulence, but it can be challenging to sift through the noise and thoughtfully separate from the herd. We believe we are only at the beginning of this valuation change, so companies should be prudent and patient with an eye toward risk mitigation.

As industrial valuations come back down to earth, investors who were prudent during the market frothiness will be well positioned for this changing market.

Copyright ©2023 by Institutional Real Estate, Inc.

Material may not be reproduced in whole or in part without the express

written permission of the publisher.

###